Make sure you help JavaScript if it is disabled in your browser or obtain the facts as a result of the one-way links provided below.

February twelve, 2021

Federal Reserve Board releases hypothetical eventualities for its 2021 bank pressure assessments

For release at nine:15 a.m. EST

The Federal Reserve Board on Friday introduced the hypothetical eventualities for its 2021 bank pressure assessments. Very last 12 months, the Board observed that substantial banking institutions were generally effectively capitalized underneath a variety of hypothetical functions but because of to continuing financial uncertainty put constraints on bank payouts to maintain the strength of the banking sector.

The Board’s pressure assessments aid make sure that substantial banking institutions are capable to lend to households and enterprises even in a severe recession. The workout evaluates the resilience of substantial banking institutions by estimating their personal loan losses and funds levels—which present a cushion from losses—under hypothetical recession eventualities that lengthen 9 quarters into the potential.

“The banking sector has provided essential help to the financial restoration in excess of the past 12 months. Though uncertainty remains, this pressure test will give the general public further facts on its resilience,” Vice Chair for Supervision Randal K. Quarles claimed.

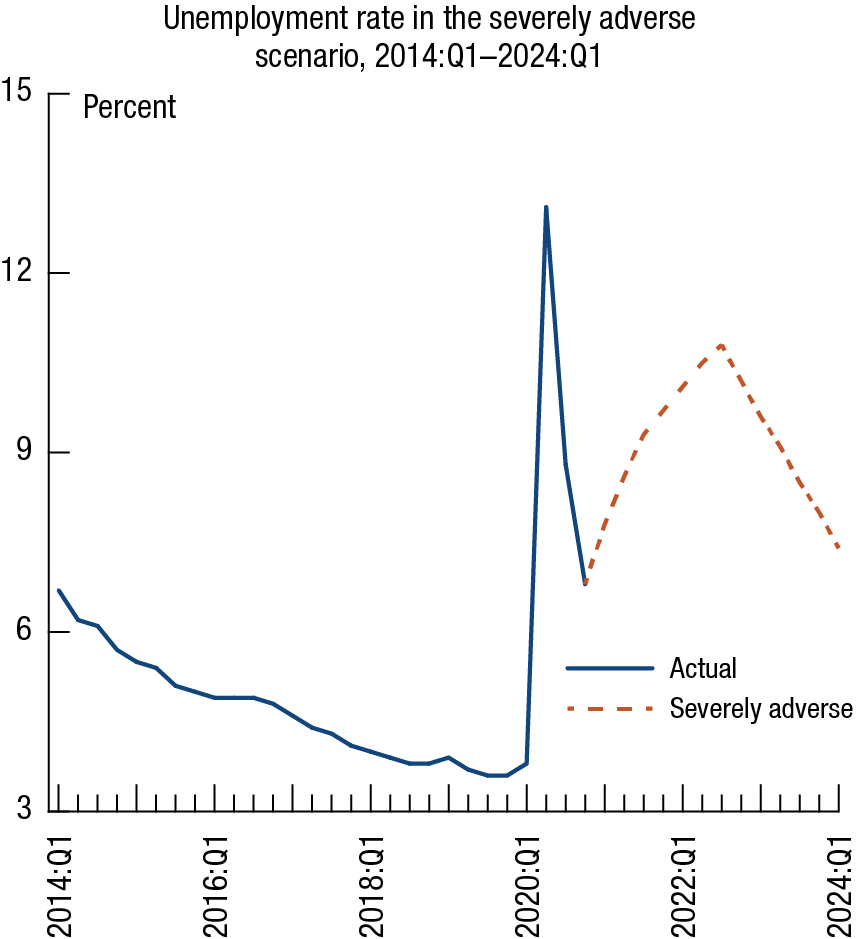

The hypothetical recession starts in the initially quarter of 2021 and functions a severe world wide downturn with substantial pressure in commercial real estate and company personal debt markets. The U.S. unemployment amount in the “seriously adverse” scenario rises by 4 percentage points from its setting up place, reaching a peak of ten-three/4 % in the third quarter of 2022. Gross domestic products falls 4 % from the fourth quarter of 2020 as a result of the third quarter of 2022, with asset price ranges dropping sharply, like a 55 % drop in fairness price ranges. The chart below displays the path of the unemployment amount:

This 12 months, 19 substantial banking institutions will be topic to the pressure test. Smaller sized banking institutions are on a two-12 months pressure test cycle but can decide in to this year’s test and need to do so by April five. Financial institutions with substantial trading functions will be examined from a world wide sector shock part that stresses their trading, non-public fairness, and other good benefit positions. Additionally, banking institutions with substantial trading or processing functions will be examined from the default of their premier counterparty. A table below displays the components that would apply to just about every bank, as effectively as determining which banking institutions are on a two-12 months cycle, primarily based on information as of September 30, 2020.

The eventualities are not forecasts and the seriously adverse scenario is significantly extra severe than most current baseline projections for the path of the U.S. economy underneath the pressure testing interval. They are built to evaluate the strength of substantial banking institutions during hypothetical recessions, which is specially correct in a interval of uncertainty. Every scenario consists of 28 variables covering domestic and international financial activity.

| Bank | Subject matter to 2021 pressure test | Can decide in to 2021 pressure test | Subject matter to world wide sector shock | Subject matter to counterparty default |

|---|---|---|---|---|

| Ally Economic Inc. | X | |||

| American Express Organization | X | |||

| Bank of The usa Corporation | X | X | X | |

| The Bank of New York Mellon Corporation | X | X | ||

| Barclays US LLC | X | X | X | |

| BMO Economic Corp. | X | |||

| BNP Paribas United states of america, Inc. | X | |||

| Money A person Economic Corporation | X | |||

| Citigroup Inc. | X | X | X | |

| Citizens Economic Group, Inc. | X | |||

| Credit score Suisse Holdings (United states of america), Inc. | X | X | X | |

| DB United states of america Corporation | X | X | X | |

| Find out Economic Products and services | X | |||

| Fifth Third Bancorp | X | |||

| The Goldman Sachs Group, Inc. | X | X | X | |

| HSBC North The usa Holdings Inc. | X | X | X | |

| Huntington Bancshares Included | X | |||

| JPMorgan Chase & Co. | X | X | X | |

| KeyCorp | X | |||

| M&T Bank Corporation | X | |||

| Morgan Stanley | X | X | X | |

| MUFG Americas Holdings Corporation | X | |||

| Northern Rely on Corporation | X | |||

| The PNC Economic Products and services Group, Inc. | X | |||

| RBC US Group Holdings LLC | X | |||

| Areas Economic Corporation | X | |||

| Santander Holdings United states of america, Inc. | X | |||

| State Street Corporation | X | X | ||

| TD Group US Holdings LLC | X | |||

| Truist Economic Corporation | X | |||

| UBS Americas Keeping LLC | X | |||

| U.S. Bancorp | X | |||

| Wells Fargo & Organization | X | X | X |

Very last Update:

February twelve, 2021

More Stories

How to E-A-T Ethically with Digital PR

What is a marketing plan? Create your 7 step plan [Free guide]

Important Facts You Should Know about Email Marketing